|

Table des matières

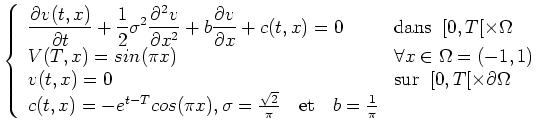

1 A parabolic problemThe following problem :

have

sigma = sqrt(2)/%pi; b = 1/%pi; L=1; T=1; hmax= sigma^2/abs(b); // state step must be lower than hmax pmin=ceil((2*L)/hmax)+1; p=maxi(pmin,20); // number of discretization points x = linspace(-L,L,p) ; // discretization points x = x(2:$-1) ; // remove boundary points. h=x(2)-x(1); // state discretization step.

sigma = sqrt(2)/%pi; b = 1/%pi; L=1; T=1;

hmax= sigma^2/abs(b); // state step must be lower than hmax

pmin= ...

p=maxi(pmin,20); // number of discretization points

x = linspace(-L,L,p) ; // discretization points

x = x(2:$-1) ; // remove boundary points.

h=x(2)-x(1); // state discretization step.

alpha = ..

beta = ..

gama = ..

n= p -2 ; // Approximate the diffusion operator

Ah= diag(beta*ones(1,n))+diag(gama*ones(1,n-1),1)+...

diag(alpha*ones(1,n-1),-1) ;

theta = ...

dtmax = ... // max time step

delta = dtmax/2;

q= ... ;

delta = ...

t = linspace(0,T,q+1); // discrete time

Bmh= ...

Ch= ...

// final condition.

deff('[y]=f(x)','y=...')

fh = feval( x' , f);

// instantaneous cost.

deff('[y]=g(x,t)','...') ;

c=feval(x,t,g); // la fonction \(c(t,x)\) }

v=zeros(n,q+1);

v(:,q+1)=fh ; // initialisation de \(v(x,T) \)}

for i=(q:-1:1) ,

v(:,i) = ...

end

plot3d(x/maxi(x),t,v/maxi(abs(v)),35,45,"X@T@V");

// compare with explicit solution.

deff('[y]=Vref(x,t)','y=exp(t-T)*sin(%pi*x)');

vref=feval(x,t,Vref);

Er=maxi(abs(vref-v))

2 finite differences for Black and Scholes equationWe will here solve by finite differences the problem :

where

which is obtained when solving the black and scholes equation in the

r = 0.05; sigma = 0.3; // constants hmax=... // max value for state step size h=.. // selected step size L=5; // x in [-L,L] // we discretize x in [-L,L] pmin= .. // min number of points p=maxi(p,100); h = L/p; x = ... // discrete points alpha = ... beta = ... gama = ... n= 2*p+1; Ah= diag(beta*ones(1,n))+diag(gama*ones(1,n-1),1)+ diag(alpha*ones(1,n-1),-1) ;

T=1; // horizon theta = 1/2; // theta used in the theta schema dtmax = ... // statbility condition delta = dtmax/2; q= ceil((T/delta)); q=maxi(q,50); delta = T/q; t = T*(0:q)/q; // discrete times S= ... R= ...

K= 40;

deff('[y]=f(x)','...') // a call or a put

fh = feval( x' , f); // the value of v at time T

v=zeros(n,q+1);

v(:,q+1)=... // final condition

// iteration

for i=(q:-1:1) ,

v(:,i) =...

end

plot3d(x/maxi(x),t,v/maxi(abs(v)))

xbasc(); i1=... i2=... xn=x(i1:i2)'; for i=1:q+1; plot2d(xn,v(i1:i2,i));end

S0=K;

d1=(1/(sigma*sqrt(T)))*(log(S0/K)+(r+sigma**2/2)*T);

d2=d1-sigma*sqrt(T);

call_price=S0*cdfnor("PQ",d1,0,1)-K*exp(-r*T)*cdfnor("PQ",d2,0,1);

put_price=-(S0-K*exp(-r*T))+(S0*cdfnor("PQ",d1,0,1)-K*exp(-r*T)*cdfnor("PQ",d2,0,1));

p = ...

// compare p with the call price or the put_price.

p -call_price ...

|